Refinancing Your Alberta Home: Unlock Your Equity, Reshape Your Finances

Thinking about breaking your current mortgage to access equity, lower your payments, or consolidate debt? Get clear on the real pros, potential pitfalls, and smart alternatives — all tailored to homeowners in Alberta.

Refinancing Your Home in Alberta?

Refinancing your home can be a smart strategy to help you reach your financial goals — whether it's consolidating debt, lowering your interest rate, accessing equity for renovations, or funding major life events like a child’s education. But like any financial move, it’s important to understand the full picture before diving in.

Why Refinance?

Homeowners in Alberta typically refinance for a few common reasons:

Lower Your Interest Rate: If rates have dropped since you first got your mortgage, refinancing could help reduce your monthly payments or overall interest costs

Debt Consolidation: Roll high-interest debts (like credit cards or lines of credit) into your mortgage, simplifying your payments and potentially saving on interest

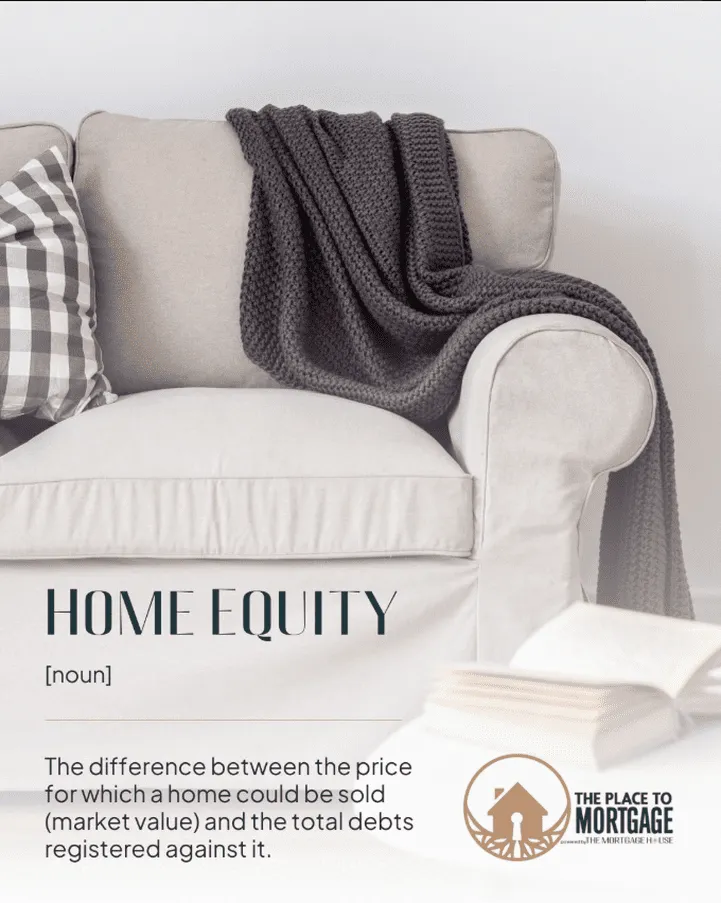

Access Home Equity: Tap into the value of your home to pay for renovations, invest in another property, or cover major expenses

Change Mortgage Terms: Switch from a variable to a fixed rate (or vice versa), shorten your amortization, or add flexible features

Add or Remove Someone from the Title: In the case of a separation or a co-signer coming off the loan, refinancing may be necessary

Potential Benefits

Lower monthly payments

Simplify multiple payments into one

Pay off high-interest debts faster

Unlock equity without selling

Improve cash flow for investment or business use

Option to renegotiate better mortgage terms

Things to Watch Out For

Refinancing isn't always the best move for every homeowner. Here are a few things to consider:

Prepayment Penalties: If you’re breaking your current mortgage term early, your lender may charge a penalty — which can be significant depending on your interest rate type (fixed vs. variable).

New Qualification Requirements: You’ll need to re-qualify under current lending rules, which may include the stress test, updated income verification, and credit assessment.

Resetting Your Amortization: Starting a new mortgage term could mean paying more interest over time if you're stretching your payments out again.

Appraisal & Legal Fees: There may be out-of-pocket costs to refinance, which could eat into your equity if not planned for.

Common Costs to Expect

Refinancing typically involves:

A prepayment penalty from your current lender if you’re ending your mortgage term early

Appraisal to confirm the current market value of your home

Legal fees for registering the new mortgage

Discharge fees to release the old mortgage from title

Possibly title insurance, depending on the lender

We always recommend a side-by-side cost-benefit analysis so you know exactly what you're gaining versus what you're spending.

Alternatives to Refinancing

Refinancing is just one tool — here are a few others to explore, depending on your situation:

Home Equity Line of Credit (HELOC): Flexible access to your equity without replacing your entire mortgage.

Blended Mortgage: Keep your current mortgage and blend it with a new one at a weighted interest rate.

Second Mortgage: Separate loan secured against your home — useful short-term, but typically at a higher rate.

Reverse Mortgage (for seniors 55+): Access equity with no monthly payments — just be sure to weigh the long-term costs.

Is Refinancing Right for You?

Every homeowner’s situation is different. That’s why we at Alberta Mortgage Expert Team, we’ll do more than just crunch numbers — we’ll sit down with you to understand your goals and map out the best-fit strategy for your future.

Let’s Chat: Book a free refinance consultation and get expert advice with no pressure or obligation.

READY TO TALK?

Come meet the team and learn more about our services, expertise, and how we can help you achieve your goals.

WANT MORE DETAILED INFO ABOUT MORTGAGES AND THE MARKET?

Read our blog

ABOUT US

Certain elements of design and content are inspired by McIntosh Mortgage Team, credited for their influence.

Copyright © 2025. All Rights Reserved. Site Credit.

ALBERTA MORTGAGE EXPERT TEAM - AN OWNED AND OPERATED FRANCHISE OF THE MORTGAGE ALLIANCE NETWORK